On 14 August 2025, the Supreme Court delivered a landmark judgment in M/s Armour Security (India) Ltd. v. Commissioner, CGST, Delhi East (2025 INSC 982), clarifying when parallel proceedings under the GST regime are barred and how Section 6 of the CGST Act should be interpreted.

The ruling resolves years of confusion over the meaning of “proceedings”, “subject matter”, and the role of summons, searches, and investigations under the GST law.

The Issue

The Issue before the Court was:

Does the issuance of summons or initiation of investigation by one tax authority bar another from starting proceedings on the same matter under Section 6(2)(b) of the CGST Act?

Background of the Case

- The assessee received a Show Cause Notice (SCN) under Section 73 for FY 2020–21.

- Later, the department also issued a search order (s.67) and summons (s.70) in January 2025.

- The assessee argued that this amounted to parallel proceedings—barred by Section 6(2)(b).

- The Delhi High Court dismissed the plea, holding that summons are not “proceedings”.

- The assessee approached the Supreme Court, leading to this authoritative ruling.

Supreme Court’s Analysis: Issue-Wise

1. Are summons “proceedings” under Section 6(2)(b)?

Answer: No.

- The Court held that search, seizure, or summons are investigative tools, not adjudicatory proceedings.

- “Proceedings” formally begin only with the issuance of a Show Cause Notice (SCN).

- Therefore, summons cannot be challenged as “parallel proceedings”.

2. What counts as the “same subject matter”?

Answer: Narrow definition.

- The subject matter is the specific tax liability, deficiency, or contravention being adjudicated.

- The Court laid down a two-fold test:

- Are both authorities pursuing the same liability/offence on the same facts?

- Is the relief/demand identical?

- Only when both answers are “yes” does the bar under Section 6(2)(b) apply.

3. What is an “order” under Section 6(2)(a)?

Answer: Broad construction.

- “Order” includes every kind of order passed under the Act—not just final adjudication.

- Once an order is passed by one authority, the counterpart must issue a corresponding order with due intimation, to maintain the single interface system.

Court’s Guidelines for Future Cases

To avoid duplication and harassment, the Court issued nine practical directions:

- Summons must be complied with—they are not proceedings.

- Assessees should intimate in writing if another authority is already seized of the same issue.

- Authorities must verify inter se to avoid duplication.

- If the subject matters differ, the assessee must be informed in writing with reasons.

- Parallel inquiries can continue until it is confirmed that both deal with the same SCN/contravention.

- If overlap exists, only one authority proceeds; the other must transfer materials and step aside.

- If authorities disagree, the one who first initiated inquiry proceeds.

- Non-compliance with these guidelines allows the assessee to approach the High Court under Article 226.

- Assessees have a duty to cooperate fully during summons and inquiries.

The Court also directed the DGGI and CBIC to create real-time, seamless data sharing systems between Centre and States to prevent duplication and strengthen cooperative federalism.

Why This Judgment Matters

- Clarity for taxpayers: No more confusion—summons and searches are not proceedings.

- Clear test for duplication: Only identical liabilities on the same contravention trigger the bar.

- Operational discipline: Both Centre and State must now coordinate inquiries instead of running in parallel.

- Checks and balances: Taxpayers gain the right to challenge violations of these new guidelines.

Conclusion

This judgment is a watershed moment in GST jurisprudence. It balances the government’s power to investigate tax evasion with the taxpayer’s right to be free from harassment by duplicate proceedings.

By defining proceedings, subject matter, and orders clearly, and issuing a structured compliance framework, the Court has set a model for fair tax administration under GST.

Key Takeaway in short

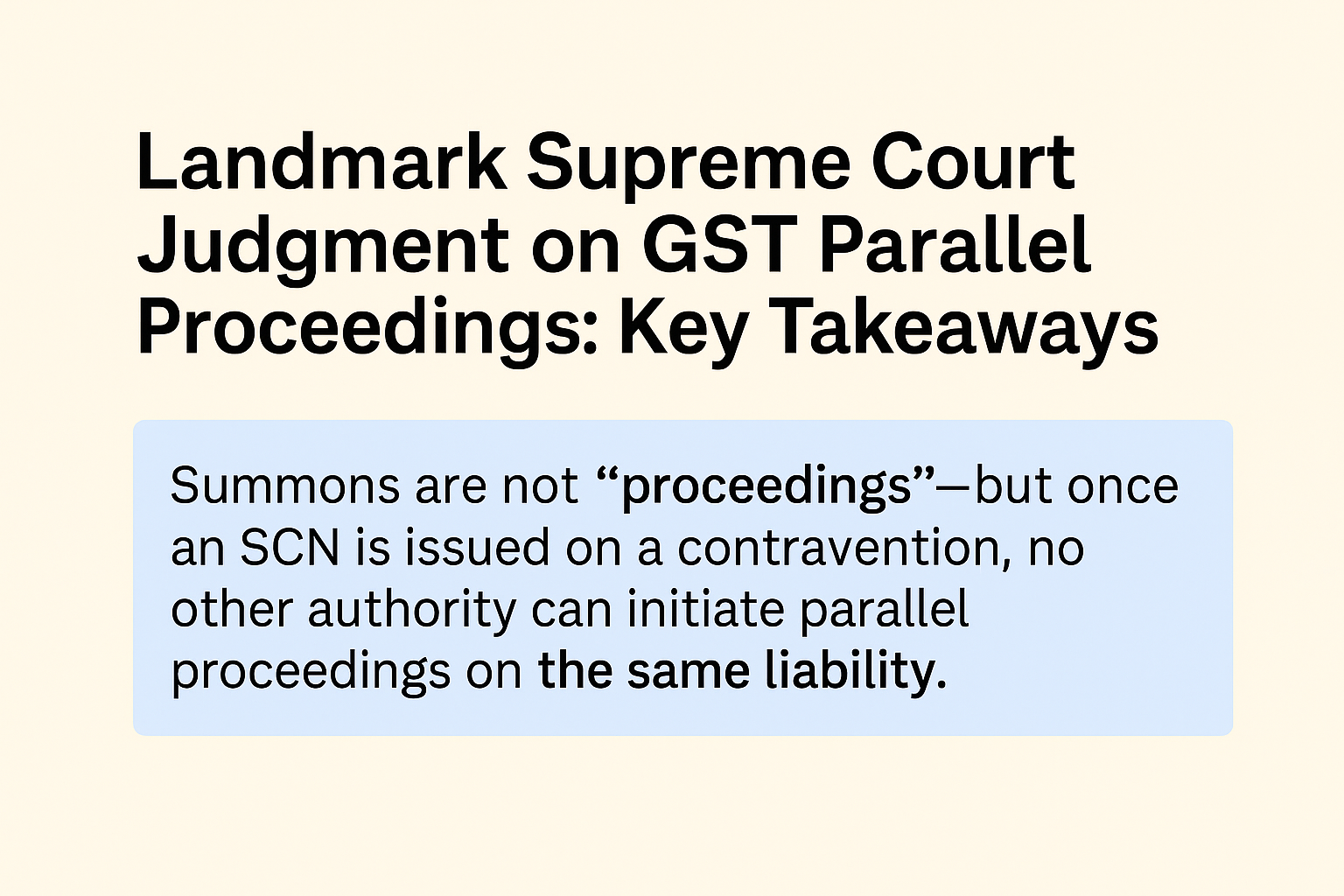

Summons are not “proceedings”—but once an SCN is issued on a contravention, no other authority can initiate parallel proceedings on the same liability.

{kind=link}

{kind=link}

Add comment