Introduction

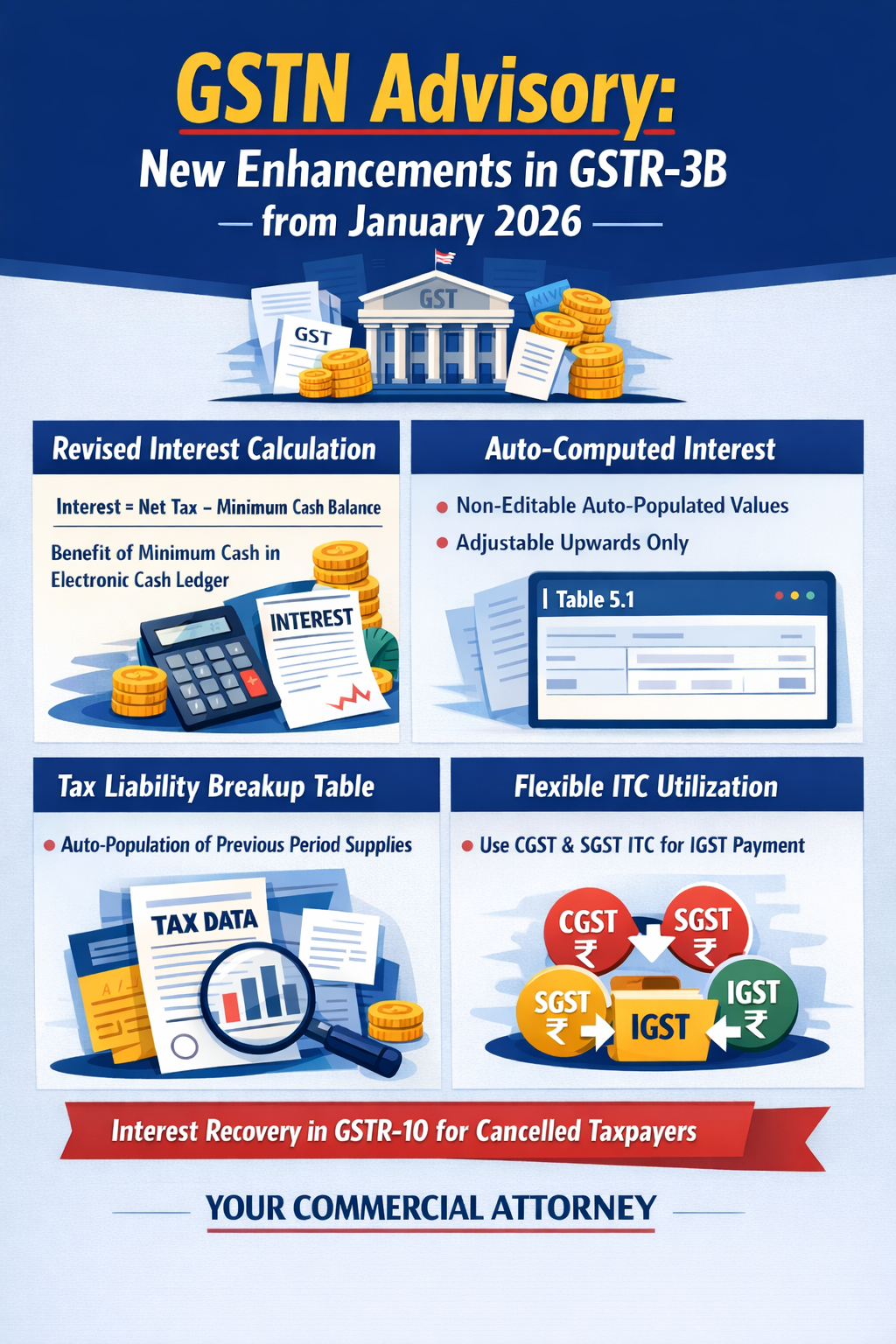

The GST Network (GSTN) has issued an important advisory introducing multiple system-level enhancements in the filing of GSTR-3B, applicable from the January 2026 tax period onwards. These changes primarily focus on interest computation, auto-population of tax liability breakup, flexible ITC utilisation, and collection of interest in the final return for cancelled taxpayers.

The objective of this advisory is to align system computation with the proviso to Section 50 of the CGST Act, 2017 and Rule 88B of the CGST Rules, 2017, while reducing disputes and improving accuracy in compliance.

1. Revised Interest Computation in GSTR-3B

What has changed?

From January 2026 onwards, the GST portal will compute interest in Table 5.1 of GSTR-3B by giving the benefit of the minimum cash balance available in the Electronic Cash Ledger (ECL) from the due date of return filing till the date of actual tax payment (offset).

Earlier, interest was often calculated on the gross tax liability, leading to higher interest demands even when sufficient cash balance was available. This system enhancement corrects that anomaly.

Revised Interest Formula

Interest = (Net Tax Liability – Minimum Cash Balance in ECL from due date to date of debit) × (Number of days delayed / 365) × Applicable interest rate

This ensures that interest is charged only on the actual unpaid portion of tax liability.

Auto-populated Interest in Table 5.1

- Interest will be system-computed and auto-populated in Table 5.1.

- The auto-populated figure is non-editable downward.

- Taxpayers can increase the amount, if on self-assessment they find that the actual interest payable is higher.

It is important to note that the system-computed interest represents only the minimum interest payable, and statutory responsibility of correct self-assessment continues to rest with the taxpayer.

2. Auto-Population of Tax Liability Breakup Table

The GST portal has also introduced auto-population of the Tax Liability Breakup Table in GSTR-3B.

What does this table capture?

This table reflects supplies pertaining to previous tax periods which are reported in the current period and for which tax is discharged in the current GSTR-3B.

How will auto-population work?

From January 2026 onwards, the system will auto-populate this breakup based on:

- Document dates reported in GSTR-1 / GSTR-1A / IFF, and

- Corresponding tax liability paid in the current GSTR-3B.

This enhancement helps in:

- Accurate reporting of period-wise tax liability

- Better reconciliation during audits and assessments

- Reduction of litigation arising from interest calculations

The auto-populated breakup can be viewed at: Login → GSTR-3B Dashboard → Table 6.1 → Tax Liability Breakup

3. Update in Table 6.1 – Flexible Cross-Utilisation of ITC

Another significant change relates to Input Tax Credit (ITC) utilisation.

From January 2026 onwards:

- Once IGST ITC is fully exhausted,

- Taxpayers will be allowed to utilise CGST and SGST ITC in any sequence to discharge IGST liability in Table 6.1 of GSTR-3B.

This system-driven flexibility simplifies tax payment and aligns with the statutory framework, reducing procedural rigidity.

4. Collection of Interest through GSTR-10 (Final Return)

For cancelled taxpayers, an important clarification has been introduced.

If the last applicable GSTR-3B is filed after the due date, then:

- Interest applicable on such delayed filing

- Shall be levied and collected through GSTR-10 (Final Return)

This ensures recovery of statutory interest even after cancellation of registration.

Key Takeaways for Taxpayers

- Interest computation is now more equitable and legally aligned

- Auto-populated values are suggestive, not conclusive

- Taxpayers must continue to self-assess and ensure correctness

- System changes reduce scope for errors, but do not dilute compliance responsibility

Disclaimer This article is prepared solely for educational and informational purposes. It does not constitute legal advice. Taxpayers are advised to refer to the applicable provisions of the CGST Act, CGST Rules, and official GST notifications for compliance and legal interpretation.

{kind=link}

{kind=link}

Add comment